When it comes to investing and personal finance, time is your friend. And the more of it you have, the better. Lately, our financial planning firm in Bethesda, MD, has noticed many clients inquiring about the best ways to kick-start their children’s retirement savings. With the traditional methods of establishing a savings account or buying individual bonds seemingly a thing of the past, people are left looking for alternatives.

One of the best investment vehicles for retirement is the Roth individual retirement account (IRA). Roth IRAs are unique in that they do not have age requirements.

This blog post will highlight the benefits of establishing a Roth IRA for kids. For a Roth IRA refresher, read this Investopedia article.

Access

One of the biggest advantages of a Roth IRA is accessibility. Anyone earning income can open one, subject to IRS income limits. To clarify, the IRS defines earned income as taxable income and wages filed on a tax return.

When it comes to a Roth IRA, kids have the same annual contribution limits as adults, which for those under 50 is $6,000 or their total earned income, whichever is less. While you can have multiple accounts, the total annual contribution cannot exceed $6,000.

It should be noted that Roth IRA contributions have income thresholds, which usually don’t matter until kids grow into higher-earning adults. If you start early and show your kids why investing is important, they can be well-established for the future.

The tough part is trying to convince a child to save their hard-earned income into a Roth IRA! The good news is anyone can contribute, so parents or grandparents can fund it if desired.

Rachel, age 16, earned $1,539 during a summer job at the local ice cream parlor.

Rachel can contribute up to her earned income for the year of $1,539.

Steve, age 20, earns $7,500 throughout the year working various jobs.

Steve can contribute up to the maximum of $6,000.

In both cases, the account could have been funded by their parents and/or grandparents. While children can’t open brokerage IRA accounts until age 18, a family member can establish a custodial Roth IRA, also called a minor Roth IRA.

The custodian (i.e., parent or grandparent) maintains control of the account and is granted decision-making power over contributions, distributions, and investment selection. Once the child reaches a required age, typically 18 or 21, the account must be transferred over to their control.

While Roth IRAs are best used as retirement savings vehicles, they do provide some flexibility:

Ability to withdraw 100% of principal contributions at any time without a penalty.

Can withdraw up to $10,000 (principal and/or earnings) penalty-free if the funds are used for a first-time home purchase.

Eligible to withdraw funds for qualified education expenses and avoid the 10% penalty. The funds are still subject to income tax on any applicable earnings.

Compounding Returns

As with most savings accounts, the earlier you start saving, the better. Compounding returns really add up over the long run. If your children or grandchildren don’t touch the contributions or earnings, they could see their account grow tax-free for 40 to 50 years! Let’s look at a few examples:

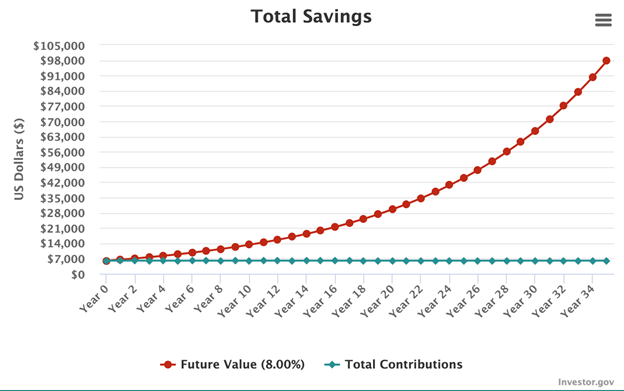

Jake, age 15, contributes $6,000 to his Roth IRA. Assuming an 8% annualized return, his Roth would be worth ~$97,755.30 when he turns 60.

Source: Compound Interest Calculator, Investor.gov.

If Jake got ambitious and contributed $6,000 annually (not adjusting for inflation) until age 60, his Roth would be worth ~$1,250,000! But it gets better. At age 59.5, Jake can tap into his Roth IRA and will owe a grand total of $0 in income tax. Far too often, investors fixate on investment returns when they should be focused on saving, and saving early!

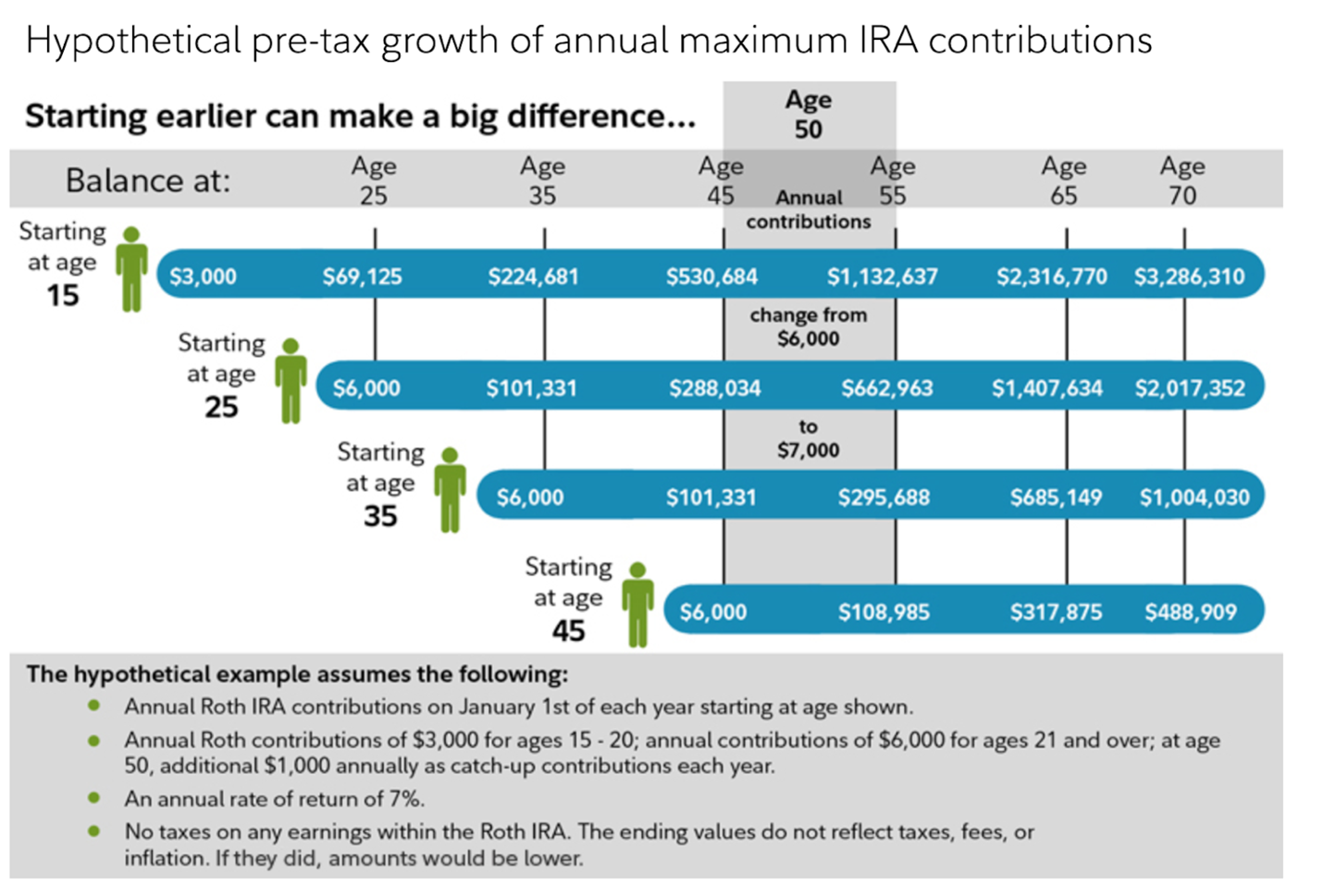

Pete, age 25, max-funds ($6,000) his Roth IRA every year until age 65, while his friend Neil starts at age 35.

The difference? Pete amasses $722,485 more than Neil! The beauty is Pete saved only $60,000 ($6,000 x 10 years) more than Neil and yet has nearly three-quarters of a million more!

Source: Fidelity.

Roth IRAs play a vital role in retirement planning. Remember, unlike traditional IRAs, a Roth is funded with after-tax dollars, which means there is no tax deduction on the contributions. This isn’t helpful for adults seeking a tax deduction, but kids tend to earn small enough amounts that their income tax bracket is already very low or even zero.

Volatility

As great as these numbers are, the only way to amass that kind of wealth is to stay invested. The longer the available time frame, the more an investor should embrace volatility.

While we know markets trend higher over time, volatility is not going anywhere. The bear markets of 2008, 2011, 2018, and 2020 were definitely not enjoyable, but those who invested during them were handsomely rewarded.

Source: Calamos.

Since 1980, the S&P 500 has experienced an intra-year drawdown of 10% or more 21 times (53%).

Since 1980, the S&P 500 has experienced an intra-year drawdown of 15% or more 12 times (30%).

The clincher? If you invested $1,000 into the S&P 500 at the start of 1980, you would be sitting on $97,885 at the beginning of this year. That’s a 9,688.58% total return or 11.83% per year!

Adding lump sums during market drawdowns would further boost these returns!

In the end, investing early and staying invested over the long run is highly recommended. While the rule sounds straightforward, far too many get tripped up along the way and don’t have the discipline to stay with the course. While investing can be emotional and difficult, working with a financial advisor can help guide you down the right path!

Discuss your situation with a fee-only financial advisor.

The commentary on this website reflects the personal opinions, viewpoints and analyses of the Divergent Planning, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Divergent Planning, LLC or performance returns of any Divergent Planning, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Divergent Planning, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Divergent Planning, LLC provides links for your convenience to websites produced by other providers or industry related material. Accessing websites through links directs you away from our website. Divergent Planning, LLC is not responsible for errors or omissions in the material on third party websites, and does not necessarily approve of or endorse the information provided. Users who gain access to third party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from use of those websites.

Divergent Planning, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Divergent Planning, LLC and its representatives are properly licensed or exempt from licensure. This website is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Divergent Planning, LLC unless a client service agreement is in place.

General Notice to Users: While we appreciate your comments and feedback, please be aware that any form of testimony from current or past clients about their experience with our firm on our website or social media platforms is strictly forbidden under current securities laws.