Rather watch Ara explain the market commentary in a video? Click here to watch.

While I recently addressed the topic of bond market volatility, I think this warrants a deeper discussion, given the massive spike in rates in October.

Even with tremendous progress in bringing down inflation, the Federal Reserve is concerned because a few of the components within the Consumer Price Index (CPI) remain elevated. Coupling this with a resilient U.S. consumer and economy, the Federal Reserve feels more work needs to be done, which has left people guessing as to what comes next. If there is one thing markets dislike, it’s uncertainty.

We are in the midst of the worst bond bear market in history. You read that correctly: IN HISTORY. I’m not saying this to be dramatic but rather to emphasize how much volatility we have endured these past few years.

Bond yields continue to push higher, as the recent unrest in the Middle East has caused a spike in oil prices, which could lead to a temporary jump in inflation. It goes without saying that human life and safety are more important than anything else, but for the purposes of this commentary, we will discuss the financial impacts.

While the Federal Reserve seems steadfast in their “higher for longer” mantra, I believe their stance will soften midway through 2024 for a few reasons.

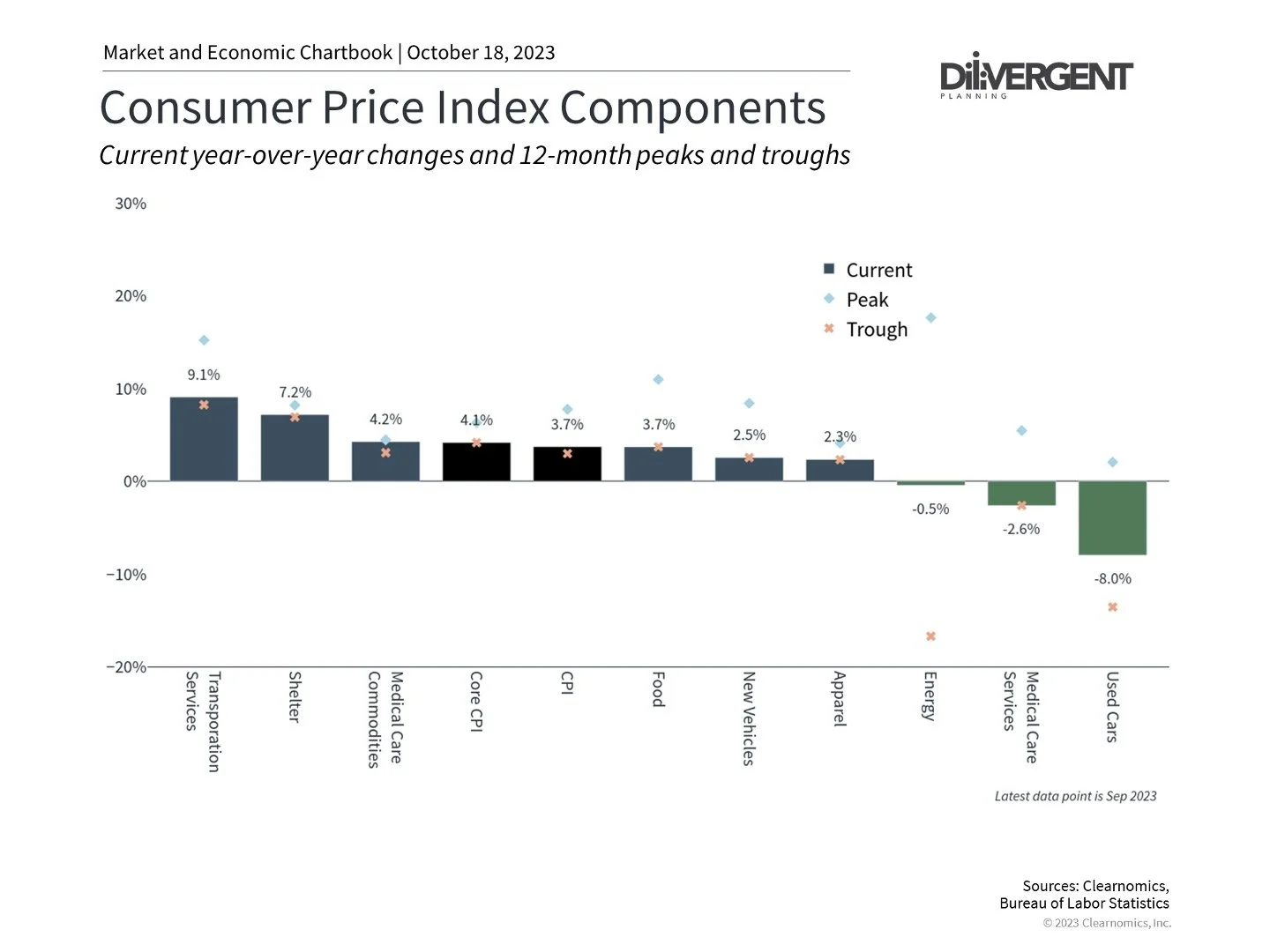

CPI

As a reminder, the CPI is composed of eight major groups. Of those, shelter is by far the biggest, comprising ~30% of the index. If you exclude shelter, inflation is not far from the Federal Reserve’s long-term mandate.

Now, I know what you’re thinking—how can we ignore something that is ~30% of the index? I’m not suggesting we do, but it’s important to note that rent is the biggest driver in shelter prices, and it’s well known there’s a 12-month lag between asking rents and CPI rents. Said another way, rent prices used in the CPI calculus lag the actual rent prices we see today. From all data points, rent has steadily decreased in the past few months.

As the chart below shows, every component, minus shelter and medical care, is well off its peak. This is important because we know that shelter prices tend to lag, so one could say that much of the fight against inflation has been resolved.

The Federal Reserve can do only so much to bring inflation down, and there are significant risks for leaving rates too high for too long. I believe the Fed is being extra cautious and does not want to make the same past mistakes.

While I appreciate the tough job they have, a more flexible mandate should be taken when most of the data points to it. If shelter prices continue to decline over the coming months, I believe the Fed will slowly pivot and take a more accommodating position with interest rates.

FEDERAL BUDGET

By now, we’re all accustomed to dysfunction within Congress. We witness it every time the debt ceiling comes around. That said, a serious problem is lurking under the surface that needs to be addressed in the near term. If not, serious negative long-term consequences could arise from inaction.

The clock on another government shutdown is ticking yet again, as Democrats and Republicans could muster only a 45-day funding bill in September. The problem lurking is the size of our national debt. Currently, total debt to GDP is ~119% and rising. This is troubling for many reasons, but even more so now, given where interest rates are.

Before proceeding, I think it’s important to clarify one thing with regard to U.S. debt. The government doesn’t repay much of its debt when it comes due. Instead, the debt is refinanced, with the debt principal kicked down the road.

The issue is that this would require additional borrowing (increasing the debt ceiling), which is exactly what we want to avoid. Now, this strategy is more feasible when interest rates are at record lows, like much of the past decade. With treasury yields nearing ~5%, this presents a new set of challenges.

I must point out that much of the rise in yields can be highly attributed to not only the dysfunction in Congress but also the Federal Reserve’s reversal on their previous policy of quantitative easing. In layperson’s terms, this means they are reducing their balance sheet of treasury and mortgage-backed securities, which is contributing to rising rates, as the Fed is no longer the main buyer.

As seen in the chart above, federal interest payments as a percentage of GDP have increased and are set to explode in the coming years unless action is taken. The good news is, as a percentage of GDP, total interest payments are still significantly lower than we experienced in the 1980s and 1990s. The issue is, without action, we could approach these levels in the next five years.

You are probably left wondering: How does the federal government plan to increase the overall debt AND pay higher interest rates? At some point, one of two things must likely occur to get things under control:

Budget cuts: These can be in the form of reducing spending, increasing taxation, altering the size of entitlement programs (think Social Security, Medicare, and Medicaid), and eliminating emergency spending programs put in place during the pandemic. While none of these is a desired outcome, some level of compromise must occur.

Interest rates: The Federal Reserve will likely have to abandon their “higher for longer” mantra and cut rates more aggressively to allow for cheaper borrowing costs. The tricky part is that cutting rates too aggressively would likely lead to a spike in inflation, which is not desired. On the other hand, leaving rates too high for too long puts the government into even more debt unless the global economy is able to flourish for an extended period.

Both actions would take place in an ideal world, but this is a very complex topic, and obtaining bipartisan support is a difficult feat these days. Difficult decisions must be made in the coming years. Interest rates are unlikely to increase much from their current levels, which is good. And while this doesn’t equate to smooth sailing, it likely means much of the worst is behind us.

Currently, many high-quality bond sectors have yield to maturities ranging from 5.1% to 6.3%, something not seen in ~16 years. Unfortunately, this does not eliminate the volatility we have seen and are likely to continue to see in the coming months, but it sets things up very nicely over the next few years.

While the information above may seem alarming, all is not lost. Volatility is part of investing. Unfortunately, we’re going through an extended period for both stocks and bonds. As we know, not all bonds are created equal and will respond differently to interest rate moves. Taking advantage of tax loss harvesting in times like this is a must. This is something we have done in the past and continue to do for clients.

In the end, bonds are a math equation. If held to maturity and no default, an investor gets their original investment in full plus interest. The twist is that between purchase and maturity, bond values will fluctuate based on various factors, interest rates being one of them.

The good news is that bonds have a “predictable” outcome, given their established maturity dates. The bad news is that many have experienced record volatility in back-to-back years. While uncertainty remains, it is important to focus on the long term.

Discuss your situation with a fee-only financial advisor.