For much of the past decade, minus a brief uptick in 2019, earning a respectable interest rate on cash was near impossible. In fact, up until the start of 2022, finding a one-year CD yielding north of 1% was considered a good deal.

As the Federal Reserve artificially drove interest rates to record lows, earning interest on cash was difficult. As with mortgage and credit card rates, rates on cash are strongly correlated with the federal funds rate. When the Fed increases its benchmark rate, interest rates across the economy tend to increase. Likewise, when the Fed decreases the benchmark rate, interest rates tend to decrease.

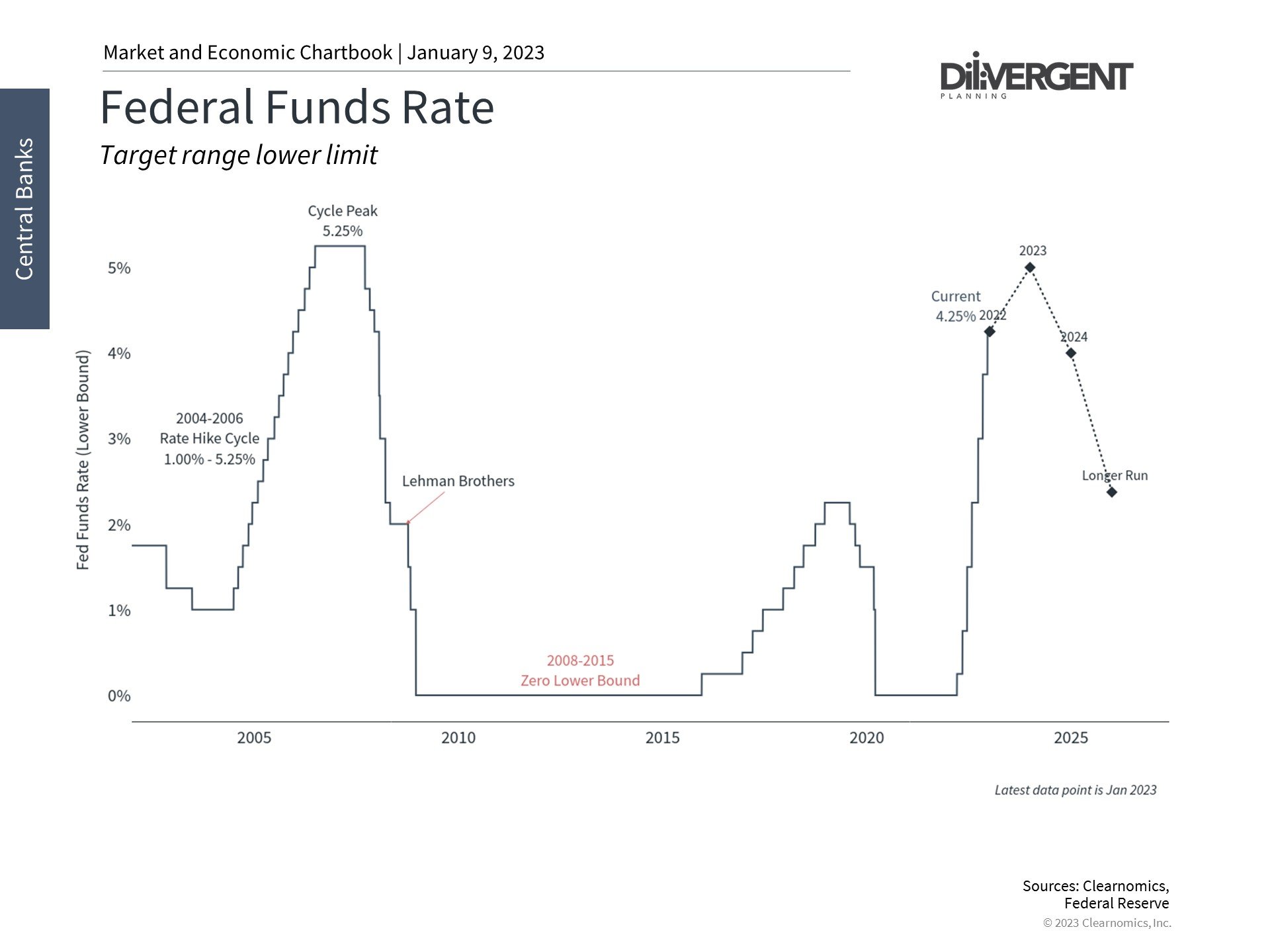

Well, what a difference a year makes!

The federal funds rate went from nearly 0% in 2021 to 4.25% in 2022! Increases of this magnitude are pretty much unheard of. Persistently high inflation was the main reason why rates increased as much and as quickly as they did.

Earning interest on your cash may help you to achieve your financial goals more effectively. This post will explore several options to earn higher interest on your cash and help you make informed decisions to help maximize your returns.

High-Yield Savings Accounts

One option is a high-yield savings account. These accounts offer higher interest rates than most traditional bank accounts while keeping your money liquid. Online banks and credit unions typically provide higher-yielding savings accounts, as these institutions generally have lower overhead and pass those savings to their customers.

Do not confuse a standard savings account with a high-yield savings account. This mistake can be costly, as the national average for traditional savings accounts is well below their high-yield counterparts. This difference can really add up over the long run.

Consider this example:

Jim allocates $150,000 of cash to a savings account at his local bank yielding .25%.

Rick allocates $150,000 of his cash to a high-yield savings account yielding 3.3%.

After one year, Rick will collect $4,575 more in interest than Jim ($4,950 - $375). The difference can be used for pleasure (e.g., vacation) or reinvested toward Rick’s other financial goals.

It should be noted that the interest rate is variable and can change multiple times throughout the year. Also, rates vary from one financial institution to another, so it’s advisable that you compare rates. In addition, you’ll want to take into consideration other factors, such as fees, minimum balance requirements, and monthly transfer limits.

Lastly, you want to choose an FDIC-insured institution to safeguard your money against the unlikely event of a bank failure. Current FDIC rules insure each depositor to at least $250,000 per insured bank. Whether you choose an online savings account or open one at your local bank, having FDIC insurance is paramount.

CD Rates

Certificates of deposit (CDs) are another option for earning interest. CDs pay a fixed rate of interest over a specific period of your choosing. The length can range from a few months to several years, and the interest rate is oftentimes higher the further out you go.

CDs are a good option for those looking for a safe and secure way to earn a higher return on cash. While CDs tend to pay a higher rate than high-yield savings accounts, they come with a major drawback: limited liquidity.

However, it is important to consider all the potential drawbacks, including minimum balance requirements, inflation risk, and early withdrawal penalties.

Minimum balance requirements: While most institutions have a minimum, these requirements are generally on the lower end ($1,000 or less).

Inflation: Since CDs pay a fixed rate over a specified period, you are susceptible to inflation risk. For example, if you buy a three-year CD at 3% and interest rates increase, your 3% rate could significantly fall behind inflation over the CD’s term.

Early withdrawal penalties: Nearly all CDs have a short-term early withdrawal penalty, which is a fee assessed if funds are withdrawn before the maturity date. The amount depends on the institution and the length of the CD, but it typically ranges between two and three months of interest.

If you are concerned about inflation, you can build a CD ladder (see the next section) to help hedge against inflation risk. Despite these drawbacks, CDs are a good option if you are looking for a fixed return and don’t need immediate access to the funds.

CD Ladders

A CD ladder is a strategy that involves investing in multiple CDs with staggering maturity dates. The goal is to generate a higher blended interest rate while maintaining flexibility and access to your funds.

Generally, longer-term CDs pay higher rates. However, there are periods like today where a one-year CD is yielding nearly the same as a three-year, so you must pay close attention.

To build a CD ladder, you allocate capital to CDs with a range of maturity dates, ranging from one to five years. This allows you to take advantage of higher CD rates without locking up all your funds for the duration. Then, as each CD matures, you can reinvest the funds into another CD or use the proceeds for your other financial goals.

A few of the benefits of using a CD laddering strategy are:

Higher rates: By allocating to a range of CDs with different maturities, you are likely to earn a higher blended rate than allocating to a single-term CD.

Flexibility: A CD ladder provides liquidity and accessibility while earning a higher return on your cash.

Inflation: Investing in a range of CDs with different maturity dates can reduce inflationary risk.

When building a CD ladder, consider your current and anticipated cash needs. This will help you determine the right mix of CDs for your portfolio and ensure you have access to your funds when needed.

Treasuries

U.S. treasuries, also known as T-Bills, are another option. The federal government issues these bonds, which are considered “risk-free” assets because the U.S. government will always repay bondholders at par when they mature. While nothing is truly risk-free, T-Bills are about as close as it gets.

Source: Worth.

Similar to savings and CD rates, T-Bills experienced a sharp increase in rates over the last 12 months.

A few benefits of T-Bills include:

Default risk: Barring a complete collapse of the U.S. government, there is no default risk.

Taxes: State and local income taxes are not imposed on the interest income generated.

Liquidity: The U.S. treasury market is widely regarded as the most liquid market in the world, making it very easy to buy and sell these securities.

Maturity dates range from a few days or up to a max of one year, and on average, the longer the maturity date, the higher the interest rate.

It’s important to note that T-Bills pay a fixed rate of interest and are issued at a discount from the par (face) value of the note. In other words, you could pay $950 to buy a one-year T-Bill that pays par value of $1,000 upon maturity. The $50 spread is your “interest” earned during the holding period.

Like CDs, T-Bills take on interest rate risk and can become less attractive in a rising-rate environment. Given that most have maturities of less than a year, the risk is minimal unless rates drastically increase in a short time.

Conclusion

You have several options for maximizing the interest rate earned on your cash. While none of these will single-handedly help you achieve financial independence, every bit counts, and a few extra thousand dollars of annual interest over the long run can add up. It is important to keep yourself informed as opportunities arise.

If you are wondering which options are best suited for you, we encourage you to discuss your situation with a fee-only financial advisor.

The commentary on this website reflects the personal opinions, viewpoints and analyses of the Divergent Planning, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Divergent Planning, LLC or performance returns of any Divergent Planning, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Divergent Planning, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Divergent Planning, LLC provides links for your convenience to websites produced by other providers or industry related material. Accessing websites through links directs you away from our website. Divergent Planning, LLC is not responsible for errors or omissions in the material on third party websites, and does not necessarily approve of or endorse the information provided. Users who gain access to third party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from use of those websites.

Divergent Planning, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Divergent Planning, LLC and its representatives are properly licensed or exempt from licensure. This website is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Divergent Planning, LLC unless a client service agreement is in place.

General Notice to Users: While we appreciate your comments and feedback, please be aware that any form of testimony from current or past clients about their experience with our firm on our website or social media platforms is strictly forbidden under current securities laws.